Five Key Points on Student Loan Interest Rates from the CBO

Yesterday, the Congressional Budget Office (CBO) released on student loan interest rates. ItŌĆÖs a treasure trove of information, and it adds new information to the debate in Congress over how to set interest rates on student loans. Here are five key points from the report.

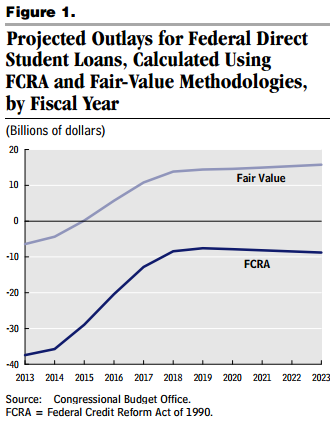

1.┬Ā┬Ā┬Ā┬Ā┬Ā The Government WonŌĆÖt Make Money on Student Loans

Student advocates and left-leaning think tanks say that the federal government makes money on federal student loans and therefore Congress should cut interest rates. The CBO has repeatedly lawmakers that those figures are wildly out of whack and it reports them only because it has no choice ŌĆō the law requires it. According to both the CBO and many financial economists, a more accurate measure would better account for risk that taxpayers bear in making the loans. From the latest CBO report:

FCRA accounting [the official rules] does not consider some costs borne by the government. In particular, it omits the risk taxpayers face because federal receipts from interest and principal payments on student loans tend to be low when economic and financial condition are poor and resources therefore are more valuable. Fair-value accounting methods account for such risk and, as a result, the programŌĆÖs savings are less (or its costs are greater) under fair-value accounting than they are under FCRAŌĆÖs rules. On a fair-value basis, CBO projects that the student loan program will yield $6 billion in savings in 2013 and will have a cost of $95 billion for the 2013ŌĆō2023 period as a wholeŌĆ”

To be sure, on a fair-value basis the loans make money for the government ŌĆō but only for the next three years. And that is a good argument for reducing rates on loans issued in those years. But then the loan program flips to a large cost of $13 billion per year, on average, starting in 2016, more than erasing any gains. Why the big change from gains to losses?┬Ā ItŌĆÖs because the government charges the same interest rate on student loans no matter what is happening to interest rates in the economy. As a result, when rates are low, the loan program generates small profits; when rates are higher, as they are projected to be in the near future, and the economy is doing better, it provides relatively larger subsidies to borrowers at a cost to the government.

2.┬Ā┬Ā┬Ā┬Ā┬Ā Current Interest Rates Poorly Target Benefits

The best way to fix what the CBO calls subsidy rate variation is to peg interest rates on student loans to interest rates in the market ŌĆō though the rates can still be held below-market. Such a plan would keep the size of the subsidy provided to students relatively equivalent, rather than providing a much smaller subsidy to students in a struggling economy. It would also reduce or eliminate any profits the government makes in low-rate years. According to the CBO:

There would be less yearly variability in subsidy rates under options that linked student loan interest rates to market rates than there is under current law.

Senate Republicans have a to do that. President Obama , too. House Republicans are . But both Republican plans only partially peg loans to market rates because they would cap interest rates at 8.25 percent. (The Senate Republican plan has a “hidden” cap that borrowers can trigger when they consolidate their loans once they leave school.) Both plans fall short of stabilizing the size of the subsidy in that regard. From the CBO report:

Imposing interest rate caps would increase the yearly variation in subsidy rates relative to options without caps. If a cap is bindingŌĆöas would occur when rates on Treasury notes are highŌĆöinterest rates on loans would be lower and the loans would receive a higher subsidy than they would without a cap.

3.┬Ā┬Ā┬Ā┬Ā┬Ā Senator Warren, Call Your Office: YouŌĆÖve Been Outspent

Here is another revealing point in the new paper. It includes a hidden estimate of the cost of Senator Jack ReedŌĆÖs to reduce interest rates on student loans such that the program generates no ŌĆ£profitŌĆØ for the government. Look at the estimated costs of the program under current law as show on the last line of Table 5 (and remember, these are under Federal Credit Reform Act accounting, not fair-value, so theyŌĆÖre not showing the true costs of the program). It shows savings of $184 billion over 10 years. The Reed proposal would effectively set the number to zero, meaning his proposal would cost $184 billion. And thatŌĆÖs not even the entire cost. That figure is for newly issued loans only. The Reed proposal would also let borrowers with old loans ŌĆ£refinanceŌĆØ into the new, lower rates his plan would set. That could easily add $50 billion, or even $100 billion, to the $184 billion figure.

Senator Warren, call your office. Senator Reed has sponsored the most expensive and most generous student loan proposal in Congress. YouŌĆÖve by hundreds of billions of dollars.

4.┬Ā┬Ā┬Ā┬Ā┬Ā Option to Lock in Rates is Valuable

The CBO paper makes an important point about a provision in the House-passed plan, which provides borrowers with variable rate loans while in school, but allows them to lock in a fixed interest rate at any point during repayment.

The option to convert variable-rate to fixed-rate loans is valuable for borrowers and costly to the government because borrowers tend to convert when they believe interest rates will increase in the future. By contrast, when all loans carry fixed rates, there is no such timing incentive for consolidation.

Critics of the House-passed plan seem to have completely this point, as have the media. Providing borrowers with variable rate loans and an indefinite option to lock in a fix rate is a big benefit, albeit one that requires much more financial literacy on the part of students and borrowers.

5.┬Ā┬Ā┬Ā┬Ā┬Ā Interest Cap or Pell Grant? Take Your Pick

Also on the issue of interest rate caps, the CBO shows how much it costs to add them to various proposals. Capping rates at 8.25 percent adds a cool $40 billion to the cost of the fixed rate plans, like the one the President proposed. That is nearly enough to stave off the for the Pell Grant program in the coming years. All of the advocates and policymakers who insist that any proposal must have a cap should consider this:

Would you rather spend $40 billion arbitrarily capping interest rates for low-, middle-, and high-income borrowers, or shoring up the Pell Grant program for low-income college students?

Issues

Related

╣·▓·╩ėŲĄ and ACCT Announce National Advisory Committee on Workforce & Economic Development