Four Corrections to Senator BlumenthalŌĆÖs BuzzFeed Post

BuzzFeedŌĆÖs lead story today is a post by Senator Richard Blumenthal (D-CT) on . But the post, despite its extensive use of graphics and charts, gets some very basic facts about the student loan issue wrong. Perhaps the most glaring of these is his claim that ŌĆ£10 million students nationwide will lose $1,000 per year from the higher [loan] ratesŌĆØ. Some students do stand to lose about $1,000 ŌĆō but over 10 years, not annually. ThatŌĆÖs a big difference ŌĆō a monthly increase of about $9 instead of $90.

BlumenthalŌĆÖs post contains a few other major discrepancies. Like the fact that 7.4 million students receive Stafford Loans, rather than 10 million that he mentions. Here are the four big problems that we spotted:

1. On July 1, only SOME student loan interest rates doubled for SOME students.

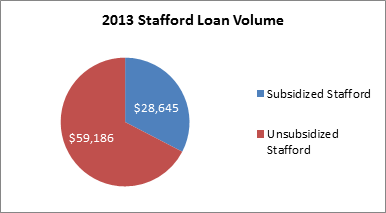

According to the BuzzFeed post, ŌĆ£your student loan rates doubledŌĆØ on July 1. True, rates did increase ŌĆō but only on a small subset of loans. The rate change only affected Subsidized Stafford loans, which made up of Stafford loan volume issued last year. And though Blumenthal cites 10 million as the number of students affected, the White House about 7.4 million students will receive Subsidized Stafford loans next year.

Source: ╣·▓·╩ėŲĄ Foundation,

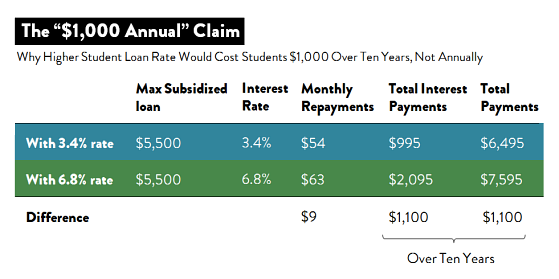

2. No, it’s $1,000 over 10 years, not $1,000 annually.

Blumenthal wrote that students will lose $1,000 annually because rates on some loans doubled on July 1. But that isnŌĆÖt accurate. The $1,000 figure refers to the additional cost to students over the life of a typical ten year loan. In other words, Blumenthal overstates the impact of the higher interest rate by a factor of ten.

HereŌĆÖs how the math works. But first, a GIF to keep your attention:

Source:

The rate change, , only affects Subsidized Stafford loans. The limit on those loans is a maximum of $5,500 per year from a studentŌĆÖs third year of college on (in the first year itŌĆÖs $3,500, and in the second, $4,500). And Subsidized Stafford loans donŌĆÖt accrue interest while the student is in school.

That means the most a student could pay on his Subsidized Stafford loan under the new rate is about $2,000 in interest, compared to about $1,000 with the 3.4 percent rate. In other words, a student will pay about $1,000 more over the 10-year life of the loan. ThatŌĆÖs about $9 more per month ŌĆō to borrow an from Allyson Klein at Education Week, less than the monthly cost of a subscription.

Source: ╣·▓·╩ėŲĄ Foundation

Blumenthal isnŌĆÖt the only one confused by this $1,000 number. We found countless other examples ŌĆō from , , , and (D-LA), among others ŌĆō of confusion about the whether the $1,000 refers to a one-year or a 10-year number.

So to clarify one more time, weŌĆÖre talking a maximum of about $1,000 per loan over the standard, 10-year repayment period for that loan. Not annually.

This confusion all probably stems from an AP report of comments made by President Obama. Obama : ŌĆ£If Congress doesnŌĆÖt act by July 1st, federal student loan rates are set to double. And that means that the average student with those loans will rack up an additional $1,000 in debt. ThatŌĆÖs like a $1,000 tax hike. I assume most of you cannot afford that. Anybody here can afford that? No.ŌĆØ AP this to mean a $1,000 annual hike.

3. The government doesnŌĆÖt profit off student loans.

Blumenthal says: ŌĆ£The government profits off these student loans, while you suffer.ŌĆØ

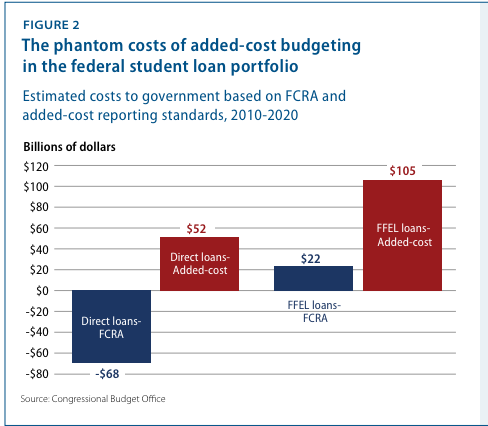

ItŌĆÖs a nice piece of rabblerousing, but itŌĆÖs wrong. In fact, the on Subsidized Stafford loans ŌĆō about a $12 loss for every $100 lent.

Looking at the cost estimates produced by the Congressional Budget Office, you might think otherwise. ThatŌĆÖs because Congress requires CBO to use inaccurate accounting plans that even the CBO says are out of whack with the true costs of the program.

The accounting practices CBO uses, which are dictated by the Federal Credit Reform Act, calculate the costs of the program using the risk factor on Treasury bonds. They donŌĆÖt account for the ŌĆō namely, the fact that borrowers are much than the entire U.S. government is to default on its debt. The Department of Education is a 23% default rate on Subsidized Stafford loans for the 2014 cohort.

Source:

CBO (and , and , and the ) recommends using instead, and even issues fair value estimates for the loan program. Under fair value accounting, the U.S. loses money on Subsidized Stafford loans most years.

4. The solution has nothing to do with banks

Blumenthal ends with a proposal he with Sen. Elizabeth Warren (D-MA) ŌĆō the Bank on Student Loans Fairness Act. It would set rates on Subsidized Stafford loans at 0.75% for one yearŌĆÖs worth of loans, the rate the Federal Reserve sets on emergency lending to banks and one that costs banks, which usually have access to much lower rates. But the plan is based on a fundamental of how student loans work. And itŌĆÖs for students if it only lowers rates for one year.

Source:

A better solution is being on Capitol Hill this week. A bipartisan group of senators, led by Sens. Joe Manchin (D-WV) and Angus King (I-ME), issued a proposal last week that is now being to gain support in the Senate. The plan will tie interest rates to the 10-year Treasury note (1.81 percent for the 2013-14 school year), plus 1.8 percent for undergraduates, 3.4 percent on graduate Stafford loans, or 4.5 percent on PLUS loans. The rates will be capped at 8.25 percent for undergraduates and 9.25 percent for graduate students and PLUS loans. ItŌĆÖs a long-term solution that will end the annual bickering that has afflicted Congress each year, provide lower rates to all students next year (not just Subsidized Stafford borrowers), and cost taxpayers nothing.

BlumenthalŌĆÖs not the only one getting some of the facts wrong ŌĆō we have a of misreported details in the student loan interest rate debate that has dominated Congress over the last two months.

Turns out just because something is published on BuzzFeed doesnŌĆÖt mean it’s true.

More ╣·▓·╩ėŲĄ the Authors

Issues

Related

Cosmetology Students Deserve Better Than Debt and Broken Promises

Quality Principles for Workforce Pell Programs