Daniel Abrahams

CEO, BeechTree

The Future of Land and Housing program developed this brief to help inform discussion at a recent on housing affordability, homeowners insurance, and megafires in California. A complementary brief focused on Florida is available here.

Climate change is reshaping housing across the United States, and Hawaii is uniquely vulnerable with its island geography, high housing costs, and heavy exposure to climate-related natural hazards. Rapidly growing threats such as wildfires, sea-level rise, and flooding are destabilizing the stateŌĆÖs already expensive housing and homeowners insurance markets. This has led to a ŌĆ£climate penaltyŌĆØ that devalues at-risk properties, while soaring premiums and loss of coverage have created a severe affordability and availability crisis, particularly for condominium associations. The State of Hawaii has enacted policies focused on increasing transparency through mandatory climate risk disclosures in real estate and has reactivated state-level mechanisms like the Hawaii Hurricane Relief Fund to provide a critical backstop for the insurance market.

These dynamics hold direct lessons for California, where a far larger housing market faces overlapping climate risks. The recent withdrawal of major insurance providers in California has destabilized local markets and intensified statewide debate around affordability, coverage availability, and the appropriate role of public insurance. This brief highlights how climate change is transforming housing and home insurance markets in HawaiiŌĆöand what policymakers in California and other states might learn from the stateŌĆÖs responses and adaptive strategies.

Hawaii faces multiple , including . These risks further strain an already limited and expensive housing market. Below are brief descriptions of the impacts of each risk and how they manifest as a risk to housing and insurance markets.

Over the past 20 years, . For example, from 2010 to 2019, Hawaii experienced a record low amount of rainfall over any 10-year period in its recorded history. More generally, climate change has increased drought frequency and intensity and, in turn, the risk of wildfire, ; the rapid spread of fire-prone invasive grass species has also contributed to heightened fire risk across the state. The 2023 Maui fires in the town of Lahaina, which killed more than 100 people and caused more than demonstrate the severity of this risk.

While there is a clear pattern of drought statewide, there are many pockets that receive large volumes of rainfall over short periods of time, such as the windward sides of the major islands. For example, in , flooding over 500 homes and causing an estimated $180 million in damage. Given HawaiiŌĆÖs mountainous terrain, these downpours dramatically increase the risk of flash flooding, landslides, and severe soil erosion.

Although direct hurricane landfalls are historically , climate change is increasing this threat. Warmer sea surface temperatures provide greater energy for storms, and shifting storm tracks are projected to increase the frequency of tropical cyclones passing near the islands. Since 1950, 25 hurricanes have passed within 200 miles of Hawaii, with only two making landfall. However, the impact can be severe: , which struck Kauai in 1992, caused more than $2.3 billion in damage (equivalent to more than $5 billion today).

As an island state, Hawaii faces a severe threat from sea-level rise, with properties in low-lying areas becoming uninsurable or prohibitively expensive to protect. Since 1960, sea level has risen between two and eight inches along HawaiiŌĆÖs shores. The National Oceanic and Atmospheric Administration (NOAA) . This will greatly increase chronic coastal erosion and create a ŌĆ£launching padŌĆØ for storm surges and tsunamis, amplifying their destructive power and allowing ocean water to penetrate further inland.

Hawaii faces an additional, non-climatic threat from lava flows, eruptions, and earthquakes. This risk is most acute on the Big Island, where designated out the areas of highest probability for impact. The 2018 K─½lauea eruption provides a stark example of the potential devastation, . Because standard insurance policies do not cover volcanic or earthquake damage, property owners in high-risk zones must seek separate, often expensive coverage, if it is available at all.

A homeownerŌĆÖs insurance policy in Hawaii typically includes the standard package of coverages: dwelling, personal property, and liability. Yet . For most homeowners, a standard policy is merely the baseline, and residents often purchase additional, specialized policies for adequate coverage against hurricanes, flooding, earthquakes, and volcanic activity. This creates a complex and expensive insurance environment in which private insurers may be unwilling to offer coverage in the highest-risk areas, such as certain lava or coastal erosion zones.

To address coverage gaps, Hawaii established the Hawaii Property Insurance Association (HPIA). Functioning as the stateŌĆÖs fair action to insurance requirements (FAIR) plan (i.e., the ŌĆ£insurer of last resortŌĆØ), HPIA is a state-mandated, nonprofit organization that provides essentialŌĆöthough often limited and more expensiveŌĆöproperty insurance to homeowners denied coverage by the private market. While HPIA provides a . Its premiums are designed to be among the highest in the state to encourage homeowners to seek private insurance first. For the most vulnerable homeowners, then, the only available option is often the most expensive.

Climate shocks are further straining the housing market and altering property values, with some rising due to shortages and others decreasing due to exposure to natural hazards. In general, climate and disaster risk have also made insurance more expensive and difficult to access.

A recent found that Hawaii homes in areas susceptible to chronic flooding and erosion experience a ŌĆ£climate penaltyŌĆØ in their valuation. The report identifies a 9ŌĆō14 percent decline in value for residential properties located in areas at risk of flooding and erosion as compared to similar, unexposed properties. According to a from the University of Hawaii Economic Research Organization (UHERO), properties in Hawaii exposed to the impacts of sea-level rise are already experiencing slower price appreciation compared to less vulnerable inland properties. These findings suggest that buyers and investors are beginning to factor long-term climate risks into their purchasing decisions. It is notable that both studies were published before the Lahaina fires and also before legislation that mandates disclosure of some climate-related hazards (i.e., SB 474), all of which further elevate climate concerns into purchasing decisions. One could reasonably expect that risk disclosure and the shock of the 2023 Maui fire to further drive devaluation.

The market is not merely ŌĆśpunishingŌĆÖ vulnerable homes with decreased values. Properties and land that are less exposed to risk or have been made to be more resilient are becoming increasingly valuable. The UHERO study mentioned above also demonstrates that homes near the coast, yet at a higher (i.e., safer) elevation, experienced a roughly 1 percent year-over-year appreciation compared to similar properties at lower elevations. This finding demonstrates that demand for coastal living remains strong, but for safer properties with less risk of sea-level rise. Though a logical response, this trend also highlights the risk of ŌĆśclimate gentrification,ŌĆÖ whereby buyers with easier or cheaper access to capital are able to purchase homes in areas less prone to disasters, or are able to afford repairs following a disaster.

Insurers are responding to climate-related and natural disaster threats by dramatically raising premiums and deductibles, especially in at-risk locations. In Hawaii, single-family homeowners are facing premium hikes ranging from 30 percent to over 100 percent, which, for a median-priced home, can translate into increases of up to $6,000 per year, depending on location and risk profile. Furthermore, in areas highly vulnerable to wildfires and coastal flooding, private insurers are increasingly choosing not to renew policies, leaving property owners with limited and expensive options such as HPIA.

The insurance crisis is particularly severe in HawaiiŌĆÖs condominium market. According to 2024 , between 375 and 390 condominium buildings in Hawaii were underinsured for hurricane risk. Faced with premium increases . Securing full coverage has become extremely difficult and costly, with premium hikes being passed directly to residents through higher association fees, in turn threatening housing affordability. Underscoring the crisis, major buyers on the secondary mortgage market, like Fannie Mae and Freddie Mac, will not purchase loans for units in buildings that are not insured to their full replacement value. This effectively .

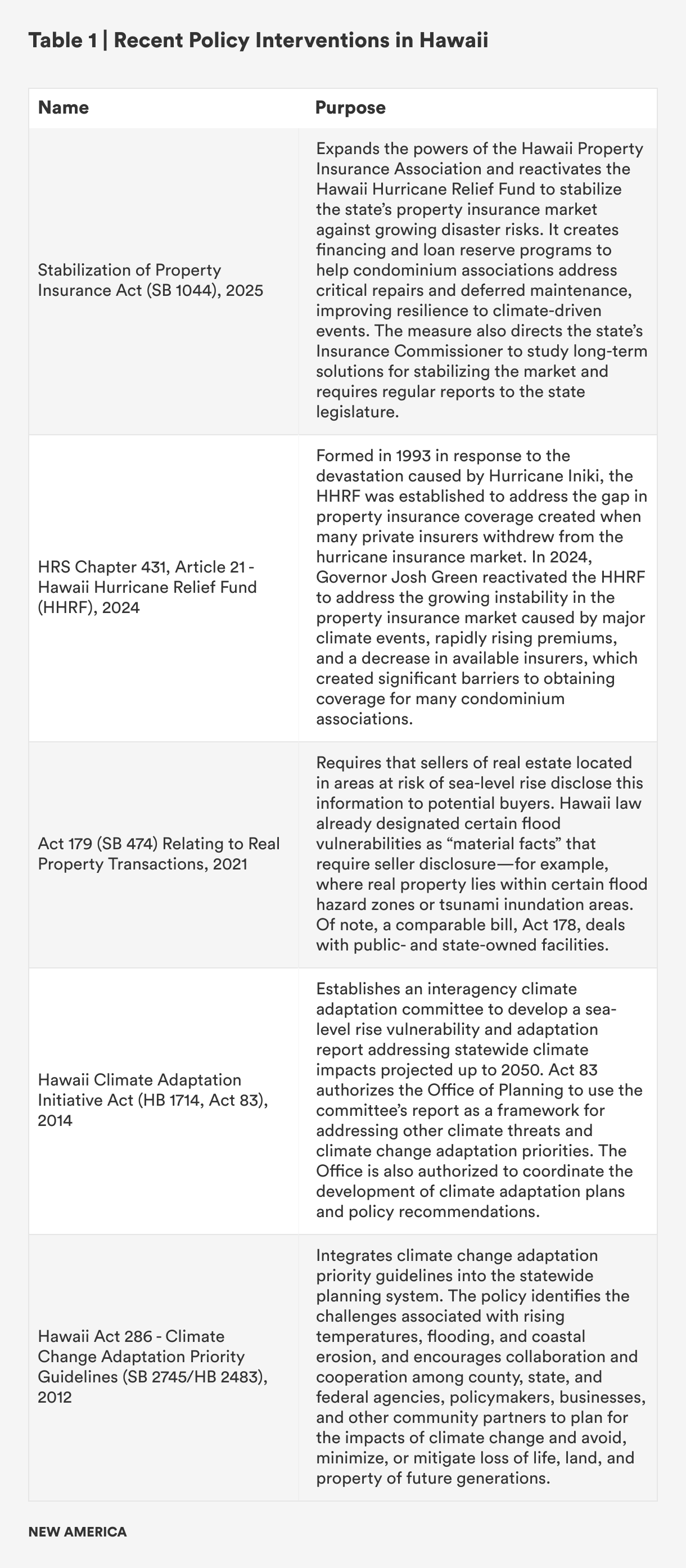

Hawaii has taken steps to address its challenges related to property values, housing affordability, and insurance access. Table 1 below provides examples of specific laws, policies, and regulations that are designed to address climate change and resilience as it relates to housing and homeowners insurance. Overall, HawaiiŌĆÖs approach is characterized by mandated planning documents, the establishment of advisory bodies, and legislation aimed at increasing transparency related to climatic and disaster-related risks.

While specific hazards differ, the underlying dynamics of market failure, insurance retreat, and the threat to housing stability are incredibly similar in California and Hawaii. California can draw several key lessons to proactively address its own escalating crisis.

Hawaii has multiple laws targeting transparency in real estate and insurance transactions (see Table 1). Additionally, the mandated creation of a statewide sea-level rise vulnerability report required counties to use this data in their planning. This established a government-validated, standardized source for climate risk that can be used in conjunction with relevant insurance and property laws and statutes. While CaliforniaŌĆÖs primary hazardŌĆöwildfireŌĆöis in many respects more complicated and less predictable than sea-level rise, steps to inform insurance markets with the best available science on risk are essential to lessen information asymmetries and identify risk mitigation measures that could in turn lower exposure for statewide insurers.

Hawaii reveals a clear ŌĆ£resilience premiumŌĆØ for safe properties and a ŌĆ£climate penaltyŌĆØ for vulnerable homes. While HawaiiŌĆÖs policies have rightfully focused on assessing and understanding risk, these dynamics create a new pressure on the existing housing affordability crisis; California faces a near-identical problem set. There are three notable pathways for climate gentrification: (1) investors target safer areas; (2) climate impacts raise the cost of living to a point where homes are only affordable to wealthy households; and (3) upgrades make a community more resilient, leading to greater demand and more expensive housing. There are numerous means to account for these risks that state and municipal governments can take, including community-led planning, providing incentives for developers to maintain or increase available affordable housing in safer areas, and, as was done in after the 2023 fires, developing community land trusts or nonprofits that hold and manage land and property to ensure long-term housing affordability.

The knock-on effects of HawaiiŌĆÖs condominium crisis offer an important, cautionary tale. The State of California should immediately review its own regulations to determine how it can facilitate the creation of alternative risk-transfer mechanisms. Solutions could include streamlining the formation of for homeowners associations (i.e., an insurance company owned by the HOA itself), , or developing a state-backed reinsurance program that specifically supports master policies for multi-family dwellings. HawaiiŌĆÖs actions show that when the market fails, the stateŌĆÖs role can evolve from a simple backstop to an active facilitator of innovative solutions.

HawaiiŌĆÖs experience demonstrates that climate change is rapidly destabilizing both housing and homeowners insurance markets. For California and other states at risk of wildfire, sea-level rise, flooding, and other natural hazards, Hawaii shows that proactive measures are necessary to mitigate housing unaffordability and financial instability. By learning from other responses, states can better protect both their most vulnerable communities and their housing from the cascading climate risks ahead.

CEO, BeechTree

Senior Policy Analyst, Future of Land and Housing